PLATONIC IDEALS:

MAKING MONEY ON CONSTRUCTION ROBOTS

The Inevitability of Automation in Construction

Construction is a $2.2T industry in the U.S. alone: vast, structurally complex, and riddled with inefficiencies and declining productivity. At the core are two intertwined challenges: a worsening labor shortage, with contractors struggling to hire, and a lack of meaningful innovation in construction equipment. Most machines haven’t advanced significantly in over 60 years, aside from gradual electrification.

We believe technology is the only scalable way to boost the productivity of the limited labor force we have, giving workers the leverage they need to build the physical world around us.

We’re convinced that one or more iconic robotics companies will emerge to serve U.S. construction. These businesses will expand the addressable market for incumbent equipment manufacturers by capturing labor spend, not just equipment spend, through automation of undesirable tasks. The opportunity in the U.S. alone is enormous.

But like most construction sites, the path forward will be messy, incremental, and ultimately transformative.

This post tackles a fundamental go-to-market question: how do you build a robotics company in an industry where machines must move constantly from site to site?

But First, Some Industry Basics: Construction 101

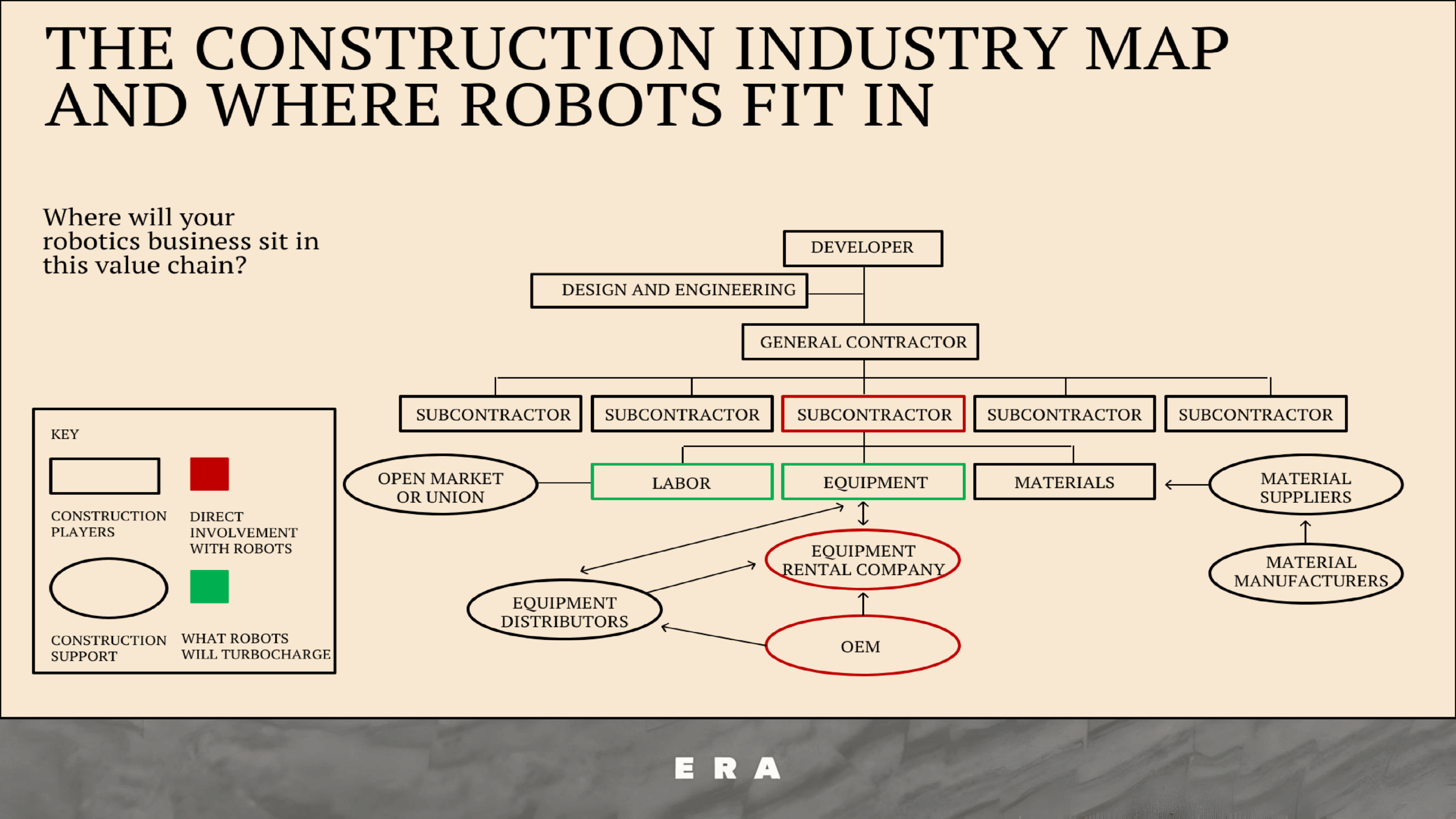

Multiple independent businesses work together to get a new building built. Below is a VERY simplified chart of how these businesses come together for a hypothetical commercial project:

(Note: most, if not all, subcontractors manage different labor, equipment, and materials.)

*Source: Chart created by Era Ventures.

For example, a developer plans to build a skyscraper. They hire an architect and engineers to design it, and a general contractor to manage construction. The general contractor, in turn, hires subcontractors — electricians, painters, plumbers, and others — to execute the work. Each subcontractor then sources what they need: hourly laborers and rented equipment to install materials.

Once their scope is complete, subcontractors release the laborers back to the market and return the rented equipment.

A key detail here: (sub)contractors run lean operations. They minimize fixed overhead by mobilizing only for the duration of a job — hiring labor and renting equipment just for that project. But the devil is in the details.

Who Owns What Construction Equipment?

While the majority of construction equipment is rented (i.e., owned by rental companies), some equipment is owned outright by subcontractors. Below is an illustrative table that summarizes the archetypes of construction equipment and who owns each.

*Source: Based on Era Ventures’ analysis and estimates.

Original Equipment Manufacturers (OEMs) like Caterpillar, Hilti, or Husqvarna have extensive catalogs, selling to subcontractors (often through distributors) or to rental companies like United Rentals, Herc, and EquipmentShare. These rental firms then supply a fragmented ecosystem of subcontractors who ultimately perform the work and assume liability for quality.

Some OEMs have market caps north of $100 billion. The three largest publicly traded equipment rental companies have market caps of $4b, $25b, and $50b respectively. The remainder of that industry is a long tail end of private regional players (EquipmentShare is a venture-backed and scaled tech-enabled equipment rental player that’s near public-ready.) Subcontractors remain largely private, fragmented, and subscale.

How Do Robots Fit into the Construction Industry Value Chain?

Given the value chain outlined above, how do robotics businesses integrate into the current structure of the construction industry?

As an emerging category, robotics companies don’t fit neatly into the traditional construction value chain. Over the past seven years, we’ve observed various experiments in this space:

Some founders position their robots as labor replacements, renting them directly to contractors on a per-job basis, much like how contractors hire labor or lease equipment. Others have taken this further by vertically integrating: bidding on projects as subcontractors and assuming full responsibility for executing the work on-site.

In our view, neither model scales effectively.

We believe the most fitting analogy for construction robotics companies is OEMs (Original Equipment Manufacturers). For these businesses to scale successfully, they must align with existing industry infrastructure rather than attempt to disrupt it. This belief stems from our understanding of the construction sector’s evolution—specifically, the way it has arrived at a relatively stable distribution of risk among stakeholders.

An Evolutionary View of Construction Equipment – Who Takes What Risks?

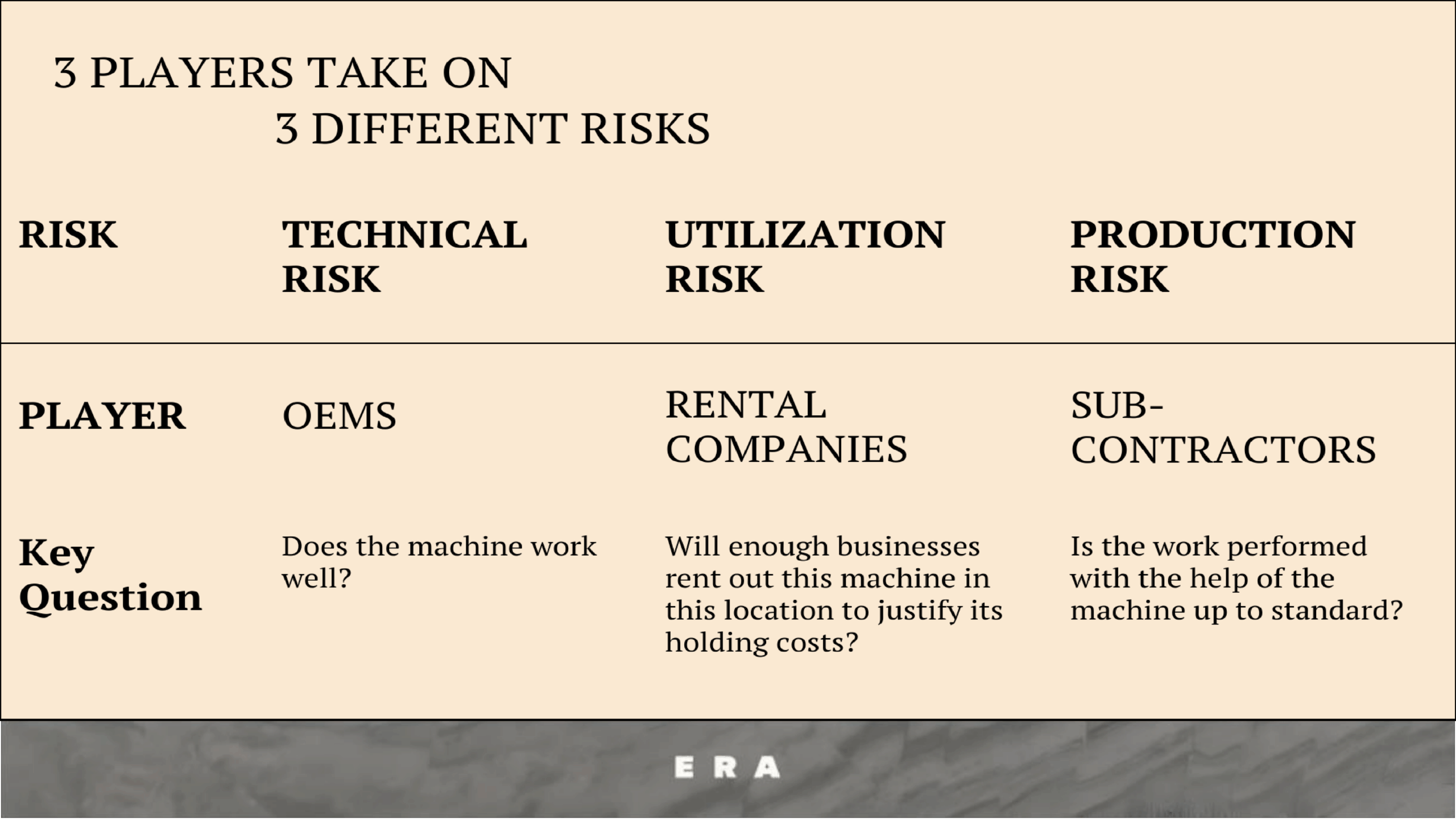

To help founders think through the business model decisions further, we identify three distinct types of risks in the construction equipment supply chain: technical risk, utilization risk, and production risk.

- Technical Risk – Does the machine work?

- Who bears the risk: OEMs

- How well do they manage the risk: Construction equipment often lasts for 15–20 years with proper maintenance. These are extremely robust, heavy-duty machines.

- Observation: It’s no surprise that cranes, excavators, and drills haven’t changed much in decades; they simply work. Further, there’s a strong disincentive to take risks in the field, hindering innovation.

- Utilization Risk – Is the machine used enough to justify its costs (capex, upkeep, and maintenance)?

- Who bears the risk:

- Equipment rental companies (e.g., EquipmentShare, United Rentals)

- Contractors who own their machines outright

- Distributors (indirectly), as they facilitate maintenance and resale

- How well do they manage the risk: The majority of construction equipment is rented, suggesting that most individual contractors can’t effectively manage utilization risk on their own. This gap justifies the $50-billion-plus equipment rental industry.

- Observation: Equipment owned directly is usually either highly utilized (e.g., cranes anchored for years) or inexpensive enough to pay down quickly (e.g., drills, small trucks).

- Who bears the risk:

- Production Risk – Is the job completed to standard?

- Who bears the risk: subcontractors, managed by general contractors (GCs)

- How well do they manage the risk: Well enough to support $2 trillion in annual U.S. construction, but not so well that you have scaled national-level players. Small and medium subcontractors frequently go bankrupt, and fragmentation reflects how hard it is to manage production risk at scale across geographies.

- Observation: No machine does 100% of a task. Humans are always needed for transport, setup, oversight, and quality control — or, as the industry calls it, “a neck to choke.”

Division of risk is everywhere if you know where to look: Delta buys planes from Boeing and Airbus, Exxon buys drills from Halliburton and Schlumberger. Construction is unique in that utilization risk is so acute that an entire industry of equipment rental companies exists to mitigate it.

This is a stable and dynamic risk management system that has evolved to support $2.2 trillion in annual construction activity. Effective founders will want to leverage this existing industry structure to scale their robotics business.

The Roboticist’s Dilemma

The project-based nature of construction, coupled with the intricate division of risks highlighted above, creates a unique go-to-market challenge for roboticists, which leaves most founders with no obvious business model to deploy on from inception through scale.

Go-to-Market Challenges:

Below are the three potential buyers of a construction robot, based on the industry map and risk categories we have identified:

- Rental companies are risk-averse. They depend on high fleet utilization and longevity, and they aren’t equipped to maintain or promote novel robots. Thus, they’re structurally the last to adopt.

- Subcontractors are fragmented and mostly own small, inexpensive equipment. They might spend ~$50k (rarely more than $100k) on new machines. A robot would need to be a direct upgrade from something they already own; introducing subscription fees for autonomy could complicate sales.

- General contractors (GCs) have historically been technology-forward partners, especially those who self-perform. But few GCs self-perform at scale. Others might see robots as a means to vertically integrate, but this requires them to fundamentally change contracting and bidding; a slow, intensive shift.

Early on, robotics founders in construction absorb all three risks. They must build the machine, secure pilot projects, and execute work on-site with hybrid crews. This “full stack” phase is a necessary evil and should be viewed as subsidized R&D, not a final business model. Full vertical integration is the most capital-intensive phase of the scale journey, and should thus be contained and minimized as much as possible.

As soon as the technology is proven, founders should focus on shedding utilization and production risks, shifting toward manufacturing and technology development rather than running a services business.

The combination of machine cost and on-site operation duration will determine whether you can sell directly to subcontractors or must rely on rental companies. Maintaining full vertical integration is theoretically possible but extremely capital-intensive and challenging to scale.

To scale, founders should aim to sell or lease machines for multi-year terms to subcontractors, and, eventually to rental companies. While other paths exist, this is the path of least resistance.

A quick aside: not all robots are created equal:

Different levels of sales friction exist for the two archetypes of machines, which we define below:

- Automate existing machines. Most have barely evolved in 50+ years. Even automating one or two workers off a crew can generate substantial savings, justifying a recurring autonomy fee.

- Create entirely new, mostly autonomous machines. Focus on trades with large labor forces and aim to reduce headcount by 30–50% by introducing a new machine where only basic tools exist.

We hypothesize that founders who automate existing machines will scale more easily than those building entirely new ones, but are very glad to be proven wrong, and to see net-new machines scale fast as well.

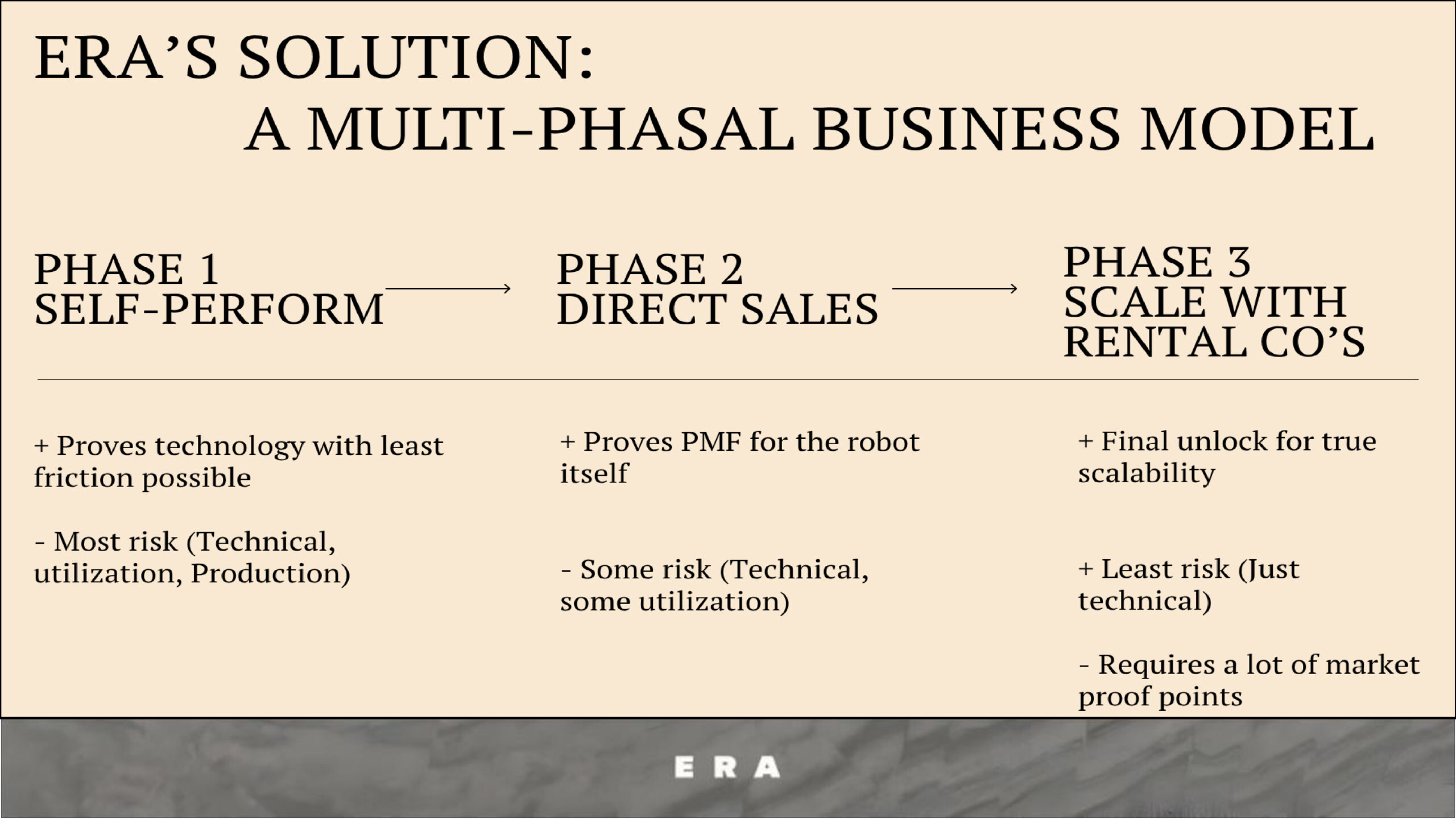

The Gradual Shedding of Risk – The Platonically Ideal Business Model Journey for Construction Robots:

We currently believe that virtually all construction robotics companies will likely need to start as vertically integrated, self-performing subcontractors, even if this model isn’t easily scalable.

We call this the “ugly duckling” phase, where the business operates as both OEM and subcontractor while absorbing all three major risks. This should be treated as a learning and refinement period lasting 6–8 quarters.

When the machine is market-ready, founders should exit production risk, focus on scaled manufacturing capabilities (technical risk), and subsequently optimize pricing (utilization risk).

The goal is to align with existing industry dynamics, not disrupt them. Once you have ~500 robots deployed, rental companies may become willing to purchase in bulk, allowing you to finally shed utilization risk and enter hypergrowth.

A Hypothetical Golden Path

We have yet to see this ideal journey fully realized. Transitioning from a services-heavy model to one that sells or leases machines outright is a long, winding process. Many founders will end up sharing utilization risk with customers, which can impact revenue predictability, but that may be acceptable at certain stages.

Nonetheless, we advocate for aiming high. After all, this series is titled “Platonic Ideals” for a reason.

Side Note: The Investor’s Dilemma

If construction robotics necessitates incremental innovation and fragmented early customers, how do you invest in the next large-scale success story?

Publicly traded giants like Caterpillar and John Deere have massive catalogs but minimal internal synergy across products. A roofing business and an excavation business don’t overlap much — limiting natural cross-sell.

We see three possible growth paths:

- Organic: Leverage one core technology (e.g., autonomy) across multiple products, even if each targets different customers. This enables scale in R&D and production while using local distributors to extend reach.

- Inorganic: Pursue M&A, consolidating profitable niche robots under one roof. However, this creates complex operational overhead and typically requires each acquired product to have strong unit economics.

- Hybrid: Combine both approaches — theoretically compelling but challenging in practice, as few companies excel at both organic product development and M&A integration.

The Time to Bring Robots to Construction Sites is Now

Scaling a construction robotics business comes with distinct business model and go-to-market challenges. Founders will navigate a tough path of selling to fragmented small businesses and evolving through a messy risk-shredding journey. That said, the potential reward is enormous and totally worth the journey.

Founders, come build robots with us!

To our fellow terminal optimists,

To the Pollyannaish few: Come build here.

But know: robots for construction

Are not for the faint of heart.

🤖🦾